If It's Broke, Fix It?

Is dollarization going to work in practice? No. Could it work in principle? Also no.

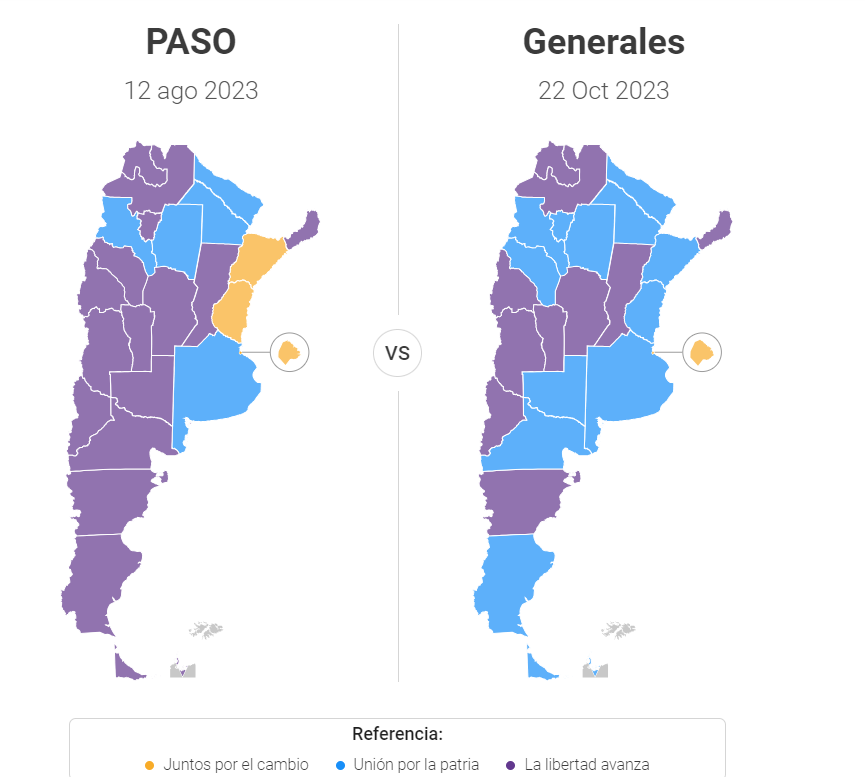

Argentina voted once again, this time for real, and it was weird in a whole different way. After the shocking outcome of the August primaries, with libertarian firebrand Javier Milei winning with a staggering 30% of the vote, the past three months have been dominated by the election campaign. Who won? What are they going to do?

The night of the long chainsaws

Election night last Sunday was different than anticipated, with Milei finishing a distant second to Economy Minister Sergio Massa, who leapt 10 percentage points to top the polls from his disappointing third place at the August primaries. Milei, meanwhile, did not gain much in terms of votes, hitting a ceiling at 30% of the electorate. The two will proceed to a runoff, with Milei leading the polls 41% to 36% - far below his 50% showing in head-to-head polling back in late August.

In detail, Milei retained his 30% of the electorate, while Massa surged from 21.5% (plus another 5.9% from a different candidate from his party) to 36.7%, and Bullrich lost around 4% of her party’s vote between August and October. Numerically, turnout increased by 3.1 million, while parties that did not cross the electoral thresshold amounted to 700.000 votes, and invalid or blank voting (generally considered protest votes) were reduced by 600.000 between rounds of voting. This 4.4 million increase in the number of ballots cast benefitted Sergio Massa primarily, who received 3.1 million more votes than in August (9.7 million, vs 6.6 million), while Milei gained an additional 770,000 supporters, alternative Peronist candidate Juan Schiaretti bagged 800,000 votes, and Bullrich lost 450,000 - finishing third in the largest province in the country and gaining 100,000 fewer votes in her party’s home turf, the Capital.

Massa, thus, was the undisputed winner of the election, taking 13 provinces (versus 9 for Milei) and turning an electoral rout into a half-decent finish. This is still the worst electoral result for a presidential election in the history of the Peronist party, and Massa faces a steep uphill struggle to secure the presidency in his own right: the economy is in a recession at the moment, while monthly inflation is steadily above 10% and the currency is in freefall in the parallel markets (briefly surpassing 1,000 pesos per dollar, versus 550 before the electoral season began), but frozen and quikcly losing value in real terms in the official market. The Central Bank has -10 billion in net assets, and most of its remaining firepower comes from loans from the Chinese government and various regional organizations or Middle East autocracies.

What, exactly, went wrong for Milei? Number one, being in the spotlight put his freakish surrogates and controversial proposals under close scrutiny. The libertarian economist and his party faced backlash due to his chaotic personal life (including the “dog dad” persona), controversial statements on human rights abuses during the 1970s, legalizing organ sales, allowing fathers to unilaterally give up on their children, and criticism of Pope Francis and other revered historical figures. Assuming he had already won cost him dearly. His party has already collapsed into infighting, blaming his alliance with controversial union leaders to make up for his overall lack of party infrastructure outside the biggest cities.

However, the general problem Milei faces is that even his close circle admit he assumed he had a “floor” of 30% of the electorate, when in reality he was at his ceiling. The barrage of negative publicity and criticism over his policy ideas, which are far outside the mainstream of Argentinian politics, made it easy for a skilled career politician like Massa to paint him as unhinged, dangerous, and extreme. Breaking through to the inherently (small C) conservative, insitutional voter base of Juntos por el Cambio (which includes a non-negligible contingent of moderate and even center left voters) might be a tough lift for Milei, particularly given that Massa seems poised to receive the bulk of the 9% of the voters that did not choose either of the three main candidates in the election. Milei, in addition, is significantly less popular among women than men, and saw his support plummet in the country’s poorest districts - meaning that, in a country with an elevated poverty rate he faces dire straits at clearing the 50% hurdle.

So Massa starts the race to the top with 37% of the vote, plus up to another 9% from independent Peronism and left wing parties, and a large share of Bullrich voters are moderate or center left: Horario Rodriguez Larreta, the centrist candidate who lost the party’s primary to Bullrich, received 11% of the vote in August.

First green is gold

The purpose of this scheme is to impose upon existing monetary and financial agencies a very much needed discipline by making it impossible for any of them, or for any length of time, to issue a kind of money substantially less reliable and useful than the money of any other. As soon as the public became familiar with the new possibilities, any deviations from the straight path of providing an honest money would at once lead to the rapid displacement of the offending currency by others. And the individual countries, being deprived of the various dodges by which they are now able temporarily to conceal the effects of their actions by 'protecting' their currency, would be constrained to keep the value of their currencies tolerably stable

We don’t really know what Massa’s economic program is going to be like, beyond “winning the election”, but we can surmise it would be the most moderate version of a stabilization program possible: FX adjustments, cutting spending, moderate tax reforms. But what would Milei do?

His signature proposal (crazy shit nonwithstanding) is dollarization, which means, roughly speaking, replacing the national currency with the US dollar. The Supreme Court has weighed in to say that it would be unconstitutional, and his advisors have walked it back to something called “currency competition”, where the dollar is legal tender and equal in status to the peso. This was something contained in Bullrich’s economic program to some extent as well, and is predicated on the idea of Gresham’s Law: that “bad currency” drives out “good currency”. Friedrich Hayek, going off this, proposed a system to allow private entities to issue their own currencies, backed purely by trust in competition. There would be a legal obligation to convert the good currency into the bad one, at flexible rates - which means that, to prevent arbitrage, currencies would have to stabilize against each other.

Whether or not more than once currency would exist at once is contentious but not especially relevant, but the point is that society would dollarize one way or the other. The currency competition framework is, in the binary of “dollarization” versus “status quo”, exactly 0.5 - it could result in a stable economy that deals entirely in pesos, whose value is sustained by trust in parity to the dollar, an economy that deals entirely in dollars, whose stability comes from trust in the dollar, or a partial scenario. This part is crucial: it is likely that a partial dollarization scenario would end with incomes in pesos and liabilities in dollars.

This is roughly equivalent to what happened during the 1990s, under the so called “Convertibility Regime”: a peso was legally worth one dollar (at a fixed rate), which resulted in stable and low inflation for most of the 1990s. The issues, fundamentally, were two: firstly, fiscal policy remained undisciplined at the subnational level, as well as pension reform blowing a gigantic hole in the national budget (due to the genius privatization scheme consisting of “paying for all the pensions” while not collecting any of the revenue). Secondly, the real exchange rate became persistently high, resulting in an increasingly uncompetitive economy and an external sector that dragged demand down. The issue is that, to offset the large external and fiscal imbalances, both households, businesses, and the public sector needed to borrow at astronomical rates - in US dollars. This meant that a devaluation of the currency would have resulted in a gigantic recession, and also that interest rates needed to be higher and higher to preserve the supply of loans funds, depressing the economy further. After a series of shocks, the currency regime unraveled, and the economy entered a tailspin in late 2001 and suffered its worst recession in history in 2002 (a still unbeaten decline of 10.9%, versus 9.9% during COVID).

The main risk of dollarization, fundamentally, is its very main benefit: it’s very hard to unravel. This results in credibly low inflation, but the problem is very evidently that inflation can be too low. Persistently weak demand (ask China) is a real concern, and dollarizing the economy results in a complete abandonment of any tools to alleviate it - monetary policy is definitionally nonexistent, and fiscal policy is severely constrained by willingness to borrow. The external sector, at the same time, completely overtakes monetary management, since the supply of money is fundamentally determined by availability of hard currency. The Impossible Trinity becomes the one-way street to currency controls, which everyone and their mother agrees have been generally bad for Argentina’s economy over the last decade. An economic recession could become a prolonged depression because of an absence of any commitment devices to alleviate it - exactly what happened with the gold standard.

This brings us into another quandary: what problems does dollarization solve, exactly? Well, the Hayek text about private currencies has an answer “Inflation is made by government and its agents. Nobody else can do anything about it”. The diagnosis is that inflation comes from exaggerated reliance on seigniorage revenue by the Treasury, which results in higher and higher price growth. This is unambiguously correct. However, dollarization doesn’t actually solve the issue of unrestrained fiscal policy. If the government could credibly commit to not fund the fiscal deficit by issuing currency, then it could lower inflation drastically with any monetary regime. Conversely, no monetary regime is stable if the fiscal authorities cannot commit to restraint. Dollarization is not the same as fiscal restraint, and it just guarantees that the burden of repayment will translate as lower output and not higher prices. Milei’s advisors openly admit to this, and instead cite that disinflation from dollarization as a political cudgel for all further reform plans, including fiscal, but once again, any credible and successful stabilization plan accomplishes this.

Getting his bag

How, exactly, would Milei implement dollarization? Well, there’s three options.

The first is that they would create the conditions for everyone to bring their US dollars into the formal sector, mainly by dollarizing without any dollars but with iron-tight financial reforms. This works for a very simple reason: Argentinians hold 300 billion in USD cash for a variety of inflation related reasons (and also “the government taking everyone’s money” reasons). The money is technically unregistered, but channeling it into the financial system could work - Mauricio Macri’s government “cleaned” around USD 110 billion, more than enough to dollarize. Since people hold USD cash as savings, the country’s banks wouldn’t face a run if sufficiently credible. There’s also a variable where the government takes everyone’s dollars and replaces them with government bonds (aka the Bonex Plan from back in the 1990s), and it’s one of the reasons nobody in Argentina trusts banks anymore.

The second option is to create a fund to convert all of Argentina’s pesos into US dollars, in exchange for a bunch of state-owned assets. The Central Bank has some Treasury bonds, the government owns a few assets, and there’s state-owned companies valued in the billions. The idea would be that the fund would stabilize the currency, and foreigners would sweep in to get the assets. But if they don’t, then the economy wouldn’t have sufficient currency to operate, resulting in a gigantic bank run and/or a complete collapse of the banking system - not pretty!.

The last option is one where Milei’s team turns the entire money supply of the country into US dollars. Right now, around ARS 29 trillion must be rescued, which at the official exchange rate of 350 ARS/USD, adds up to around 90 billion dollars. This is composed of the entirety of the Central Bank’s liabilities with banks (USD 37 billion), as well as the entire money supply (USD 21 billion). Depending on the specificities of financial reform, you would also need to rescue the M3, or a further USD 25 billion. In terms of assets, the outlook is grim: reserves are of USD 25 billion, but net reserves are - 10 billion. The Central Bank holds 60 billion of bonds with actual value (Treasuries), and 70 billion of worthless ones. The government holds 6 billion in assets seized from pension funds in 2007. If the bonds are valued at a third of their face value, then you have around USD 16 billion to dollarize, meaning you’d have to get financing for USD 70 billion or so.

Here’s the fun, however. At a higher exchange rate, you need fewer US dollars - for example, at the mid-September rate of 700 pesos per USD, you’d need half as much money (USD 35 billion). At 1000 pesos, which the exchange rate hit last week, you would have to borrow 24 billion. At 2000 pesos, you would only need 12 billion, which is as much cash as the Central Bank holds (gold + bank reserves). Of course, an exchange rate of 2000 pesos per dollar would be tantamount to hyperinflation, since both forecasters and USD futures predict an exchange rate of 1000 at most by December. Hyperinflation is very poorly understood, but in general, it results from prices growing a lot. The core idea here is that expectations of future inflation get so out of hand that everyone keeps raising prices constantly in a very short timespan, usually within weeks or days. If a dollarization is announced ahead of time, then people would start shedding their pesos and replacing them with dollars, pushing the exchange rate up and up to the market level. Since this would entail a gigantic upwards lurch in the real exchange rate, it would also entail a massive increase in prices, and therefore a brief hyperinflation before the peso is abandoned completely. Meanwhile, if not announced previously, it would translate as a recession as all prices readjust to a new currency. A recent paper by MIT economist Ivan Werning theorizes that, if the Central Bank has enough reserves at the dollarization rate (that is, equivalency between dollars and pesos), then nothing happens. However, if there aren’t enough reserves, then there’s a sudden, gigantic recession and a sharp drop in inflation - 2002 in reverse. This recession comes, surprisingly, in a form alike to a “sudden stop”, an external-sector motivated recession the likes of which Russia suffered last year.

The Ecuadorian experience is interesting. Ecuador suddenly dollarized in January 2000, replacing the national currency (the sucre) with the US dollar at a rate of 25,000 to 1. In the year prior to dollarization (1999), inflation had been 60.7%, which quickly spiked to around 100% for most of 2000, but rapidly stabilized: from 91% in december 2000 to 58.8% in March 2001, then 33.2% in June, 27.2% in September, and 22.4% in December. A year later, prices were at 9.4%, and two years after, at 6.1%. However, economic activity suffered sharply: monthly GDP dropped 25% in January alone, but quickly rebounded, growing 1.1% in 2000, and 4% for the two following years. If Argentina dollarized at 180% inflation and two and a half times the monthly inflation (4% versus 10%), it doesn’t take a genius to see that prices would grow around 300% for the peak in 2024, then quickly fall to around 50%, and then converge to US levels by 2027 or so. This is rather fast, but would also entail a gigantic cost to real wages, perhaps at their lowest levels ever.

Conclusion

Is dollarization a good idea? No. It doesn’t seem especially good at solving any issues in particular that aren’t solved by something else, and it creates a bunch of other issues, such as “possible Great Depression” if a lot of perfectly normal things happen. So like, not a great bet. Now Massa is a flakey flip flopper, probably corrupt, and his ideas will just prolong the current mediocre to bad scenario for another half a decade, so he’s not like, good. Just not completely unhinged and/or married to a genuinely bad idea. So idk, pick your poison.

Panama dollarized and has done quite well