Putting Out Fire... With Gasoline?

Why faster growth for longer could make the recession worse

You've been so long

Well, it's been so longAnd I've been putting out the fire with gasoline

Putting out the fire

With gasolineDavid Bowie, “Cat People”1 (there’s two versions so link in the footnote)

A while ago, I wrote about Friedman’s plucking model, which proposes that there’s a relationship between how deep a recession is, and how fast the economy recovers from it. There’s also an inverse view, called the “natural rate model”2, which states that how quickly the economy grows before a recession is related to how bad the recession is - a stronger economy means a worse recession. Exactly why is debatable, but it either means that companies will be in a weaker position later, or that there will be more inflation and that would eventually require a recession to bring down.

This sounds like an absolutely insane view, but it’s actually a very old one, and one held by very influential people. Several members of the Federal Reserve Board of Governors had to be convinced by Janet Yellen that faster growth during the 90s wouldn’t cause inflation because it was led by higher productivity, for instance. This might seem like a right wing belief, but it used to be really popular in the 60s: policymakers didn’t just have to bring GDP “up” during recessions, it also had to bring it “down” during expansions - to prevent the expansion making the economy worse in the future.

A primer on the business cycle

The most important thing to understand is what’s called “the business cycle”, which has absolutely nothing to do with business and everything to do with GDP.

This is a typical image of what the business cycle looks like. There’s something called a recession, which happens when people spend less money than normally, so a bunch of businesses shut down and a lot of people lose their jobs. The worst point of the recession is called the trough, and after that the economy begins recovering - i.e. getting better. Once it gets to where it was when the recession started, what’s called an expansion starts, because the economy is adding more growth, not just gaining it back. If there’s another recession, the highest moment before it starts is called the peak. Even though it’s called a cycle, very few people believe that recessions and expansions cause each other, but many believe there’s a correlation between the two.

An important related concept is potential output. Potential output measures how much the economy could make if everyone who wanted a job could get one, all businesses were running at full steam, etc. So if everthing that’s useful for making things was in use, the economy is “in full employment” (or in equilibrium, they’re the same thing) and making more of something requires resources used to make something else. Most economists agree that potential output is fixed in the short term, and that it depends on how much of the factors of production (labor, capital, and land) you have, plus how good the technology to use them is. Potential output is relevant because, during expansions, the economy grows alongside its potential path, but during recessions, it falls below it. It’s possible that the economy is no longer in a recession, but is also growing much more slowly than potential output, and that’s bad.

There’s some facts about the business cycle that most people agree on:

“Fluctuations occur in aggregate activity and not in particular sectors; cycles are recurrent but not periodic” - so recessions are the whole economy going down, not just a few sectors (though they don’t go down as much or at the same time), and recessions happen at intervals but those intervals don’t have much significance - there’s no “recession every 20 years” like with fashion trends.

“Cycles have at least two di§erent stages, expansions and contractions; once the economy enters one of the stages, it stays there for some time, so detecting turning points is important for forecasting” - it’s important to tell when a recession starts or ends because they tend to last for some time.

“There are regular and predictable co-movements between variables over the cycle that can be expressed as relative variances and lead-and-lag correlations.” - some variables usually go down before a recession, and some always go up when a recession ends, so they can be useful predictors.

“Business contractions appear to be briefer and more violent than business expansions” - recessions are shorter but deeper than expansions.

A controversial one: “the economy spends more time below potential than above it” - this means it’s more common that there’s too much unemployment than there is too little, for example.

A new one: “contractions in employment are as deep as contractions in GDP, but they’re shorter and happen later” - because it’s expensive to hire and train workers, companies tend to not want to lay them off when it seems like there might be a recession, but lays off as many as “needed” when there is one.

There’s two big theories I wanna talk about, that can be compatible with either of the three above: the forest fire theory, and the plucking model (read my full post on the plucking model here)

Forest fires

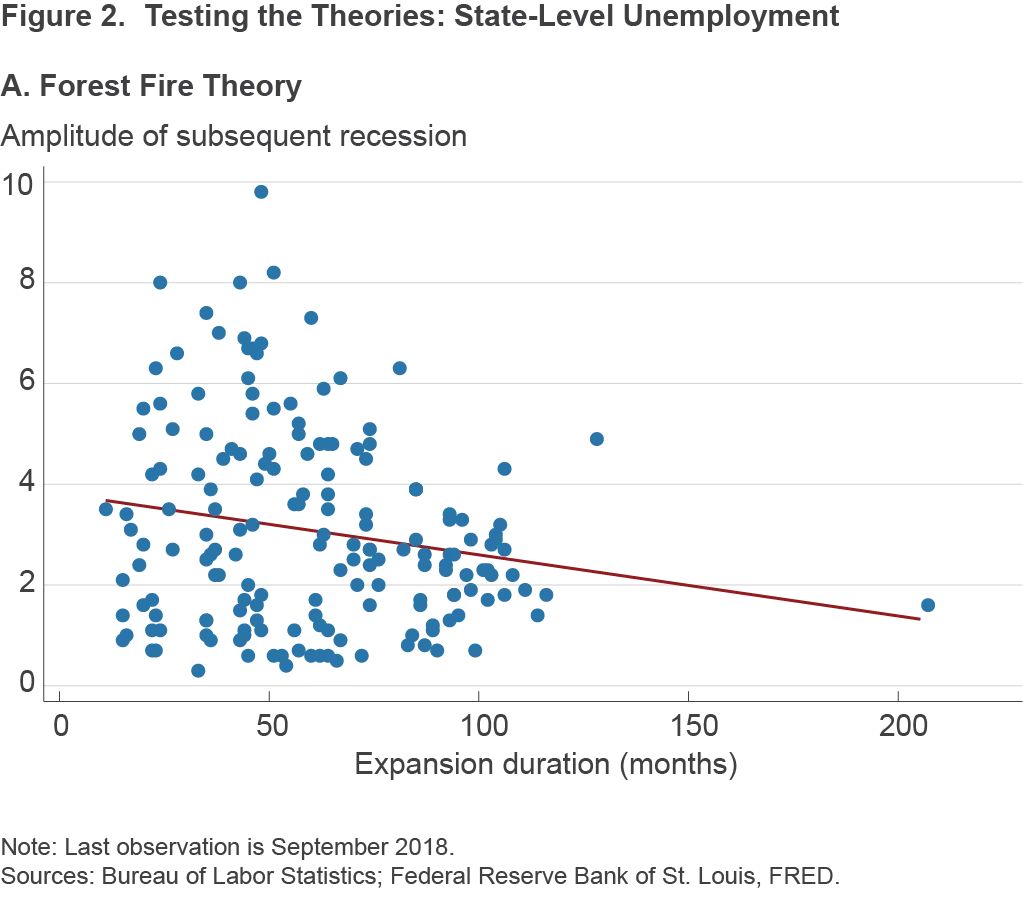

A good way to conceptualize the natural rate model is through forest fires. Forest fires are often seen as random, and because they’re very destructive, the government usually tries to prevent them. But the ways the government attempts to stop fires is by preventing any fires as soon as possible. The problem is that this allows for very dense forests full of dry leaves and dead trees, that are incredibly flammable. As a result, the longer a forest goes without fires, the worse the subsequent fire is.

A 2019 paper proposes that the economy works the same way. Imagine that the economy can either be growing or in a recession, and that it happens randomly. Also, companies can choose whether to hire workers, and the hires can be good or bad for the company. Hiring a good worker is always profitable, and hiring a bad one is profitable in expansions, but not during recessions. Assume companies and workers part ways randomly unless there’s a recession - workers just quit, or retire, or get fired for whatever reasons that don’t have to do with the economy.

If conditions are just right, most companies are going to hire some bad workers anyways, because it might be easier to get better ones later, or there’s not enough good ones to justify the hassle, or the profit gains are big enough, or recessions aren’t very likely. The problem is that, if this is the case, the longer the economy goes without a recession, the likelier it is that companies are going to have a lot of bad workers, and if a recession does come, then those companies are going to do really badly regardless of how big the recession was. And if these issues compound over a longer, bigger expansion, then long big expansions are always preceded by very bad recessions - just like forest fires.

So in consequence, governments have to do something called active stabilization policy. Stabilization is keeping the economy “in equilibrium” by making sure that there isn’t too much inflation or too much unemployment. But if the forest fire theory is true, then stabilization isn’t just fighting recessions, it’s also preventing expansions from getting too big - lest they make future recessions get too bad.

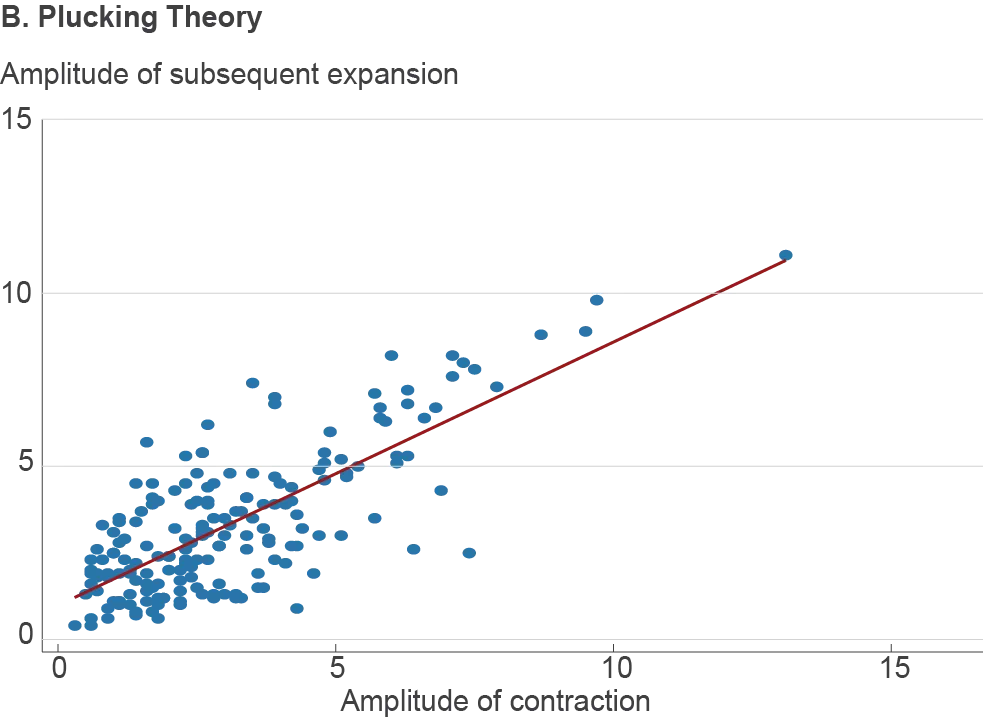

The plucking model

In the 60s, Milton Friedman proposed a theory where how much the economy grew before a recession didn’t matter, but how bad the recession was made the economy recover more quickly afterwards - unless there was a financial crisis, because those are super messy and bad. The idea is that, when GDP went below potential, it acted like a string “plucked down” and went back up, so the harder you plucked it, the faster it went up. But Friedman didn’t really come up with an idea for why.

So why is the business cycle like that? There’s some possibilities:

Labor hoarding: Companies can use old technology for a long time by hiring more workers, so they try their best to not fire anyone until they absolutely have to, and invest in the new technologies when the economy is looking better.

Capacity: Because potential output is capped and it costs money to increase it, it’s more common that the economy goes below it, but that it’s also easier to bounce back to where the economy initially was.

Stickiness: companies don’t like cutting wages or prices, so when a recession happens, they have to fire people instead - but when the economy grows, they can just pay people more.

The implication here is that stabilization policy has to be passive - i.e. you don’t do anything during expansions unless there’s inflation, and you don’t do anything about recessions unless they’re already happening.

Who’s right?

There’s two ways to be right here: the empirical evidence, and the theory.

Regarding the empirical evidence, like in my plucking model post, Friedman is right and the other people are not. Evidence explicitly comparing the two models from the Cleveland Fed finds that there’s no relationship between how long an expansion is, and how bad the recession after it gets - and the one they find, which isn’t statistically significant (i.e. can’t be ruled out to be zero) actually goes the opposite way around. Meanwhile, the relationship Friedman proposes, that a worse recession ends more quickly, is proven right - results have the correct sign, and are very significant.

The other way you can be right is theory. In this case, the theory is rational expectations, something a lot of people hate. The gist of rational expectations isn’t that it purports to describe how people act, but rather, that it states that the economy as a whole doesn’t waste information - so you can’t fool everyone all of the time. Why and how is this relevant here?

Well, active stabilization policy states that, once the economy gets strong enough, the government will gently bring it down so it doesn’t cause inflation. The problem is that, because the way the economy works changes all the time, and especially changes when government policy or the expectation thereof change, then it’s impossible to predict when a recession is going to happen based on indicators of when a recession last happened - the relationship there might have simply broken down.

Plus, even if that wasn’t a problem, then trying to smooth out the business cycle might make it even more volatile: if people can’t tell if the economy is going down because there’s an actual recession instead of the government slowing down the expansion, they’d act as if there was a recession, and then a recession would actually happen even when the economy was doing quite well - so you’d get more recessions, not fewer, and people would be worse off.

Conclusion

Don’t believe in the goofy ass idea that more people having jobs now somehow makes fewer people have jobs in the future, because it’s not true and also because it doesn’t make sense as a guide to policy anyways.

Sources

My posts on the plucking model and on rational expectations.

Business cycle data:

McKay & Reis (2008), “The brevity and violence of contractions and expansions”

Forest fire model:

Jackson & Tebaldi (2019), “A Forest Fire Theory of the Duration of a Boom and the Size of a Subsequent Bust”

The plucking model:

Evidence:

Tasci & Zevanove (2019) “Do Longer Expansions Lead to More Severe Recessions?”

Rational expectations:

Lucas (1976), “Econometric Policy Evaluation: A Critique”

Sargent (1980), “Rational Expectations and the Reconstruction of Macroeconomics”

Important question: do you think the 1982 version or the 1983 one is better? NGL anything from Let’s Dance automatically wins

Not to be confused with the natural rate theory invented by… Milton Friedman. bro.

I’ll definitely write a longer, better one at some point