(Un)productivity

"You can see the computer age everywhere but in the productivity statistics." - Robert Solow

What everyone feels to have been a technological revolution, a drastic change in our productive lives, has been accompanied everywhere by a slowing-down of productivity growth, not by a step up. You can see the computer age everywhere but in the productivity statistics.

Robert Solow

Economic growth is slowing down. Technological progress is getting harder. Populations are growing slower. Incomes aren’t keeping up with previous trends. All of these are bad. Why are they happening? And are these related?

I’ll frequently be alluding to my posts on declining birthrates, economic concentration, and a loose labor market, so I recommend checking those out!

What even is productivity?

The key item here is productivity. But what even is that? Total Factor Productivity, sometimes called Multifactor Productivity, and shortened as just productivity (or TFP) is a tricky concept. The original idea comes from Robert Solow, creator of the basic workhorse model of economic growth (the Solow Model, duh). The model is pretty simple: imagine an economy that uses some fixed combination of labor and capital to produce goods. These factors are used in various proportions and combinations to produce various amounts and types of things - like how meat and flour can make an empanada, a taco, meatloaf, etc. So if an economy is richer (in per capita terms) than another, it must either have more capital per worker, or be more efficient at turning labor and capital into goods and services. Mathemathically, this is often just a fixed constant multiplying the function that turns labor and capital into output.

If you wanted to check the sources of economic growth, you could just verify the equation by which you get GDP: growth should equal the growth of the supply of labor (i.e. the population) times its share in national income, and the growth of capital times its own share. Except this predicted growth is much lower than actual growth - and because of how the math worked out, a huge chunk of growth comes from the growth in that extra variable. Solow called this “the residue”, but we now know it as productivity.

So what does productivity measure, exactly? Basically, it’s a sort of clunky measurement of efficiency, i.e. how good the economy is at either allocating its resources between companies, or how good it is at turning “raw materials” into products. It’s NOT a measurement of innovation, although innovation frequently has a lot in common with productivity - for example, new technologies make industries run on fewer resources (improving the first kind) or at making more with less (the second kind).

The problem is that there’s other types of innovations that can’t really be captured by clunky ideas about efficiency. The most obvious example is new items, either types of capital or of product - having more things to produce from, if they’re not much more or less intensive in resources than existing ones, doesn’t change productivity. The other option is innovations that change economic activity but only slightly, such as advances in medicine that only improve quality of life, or things like switching from coal to solar energy. Or it could improve the quality of products, which is a pain in the ass to actually incorporate into models. The effects aren’t directly captured by TFP in either case.

So why is productivity growth important? The reason is that, with stable productivity (i.e. zero productivity growth), the only way to grow the economy is to use more resources (or the non-measured improvements we’ve talked about before). Over the long term, you can’t actually do that, because there’s not an unlimited amount of things in the world. For example, a lot of very poor countries (such as, say, China or India) grow at spectacular rates and then slow down - the reason is that going from very poor to somewhere in between can be accomplished by just throwing resources at a very backwards economy and growing from there, but once you moved a billion peasants into cities and gave them all electric tools and high school diplomas, you can’t do it a second time. So productivity (however it’s gotten) is, over the long term, the most reliable source of growth - just getting better and better at using your resources.

Is productivity going down - and is it actually bad?

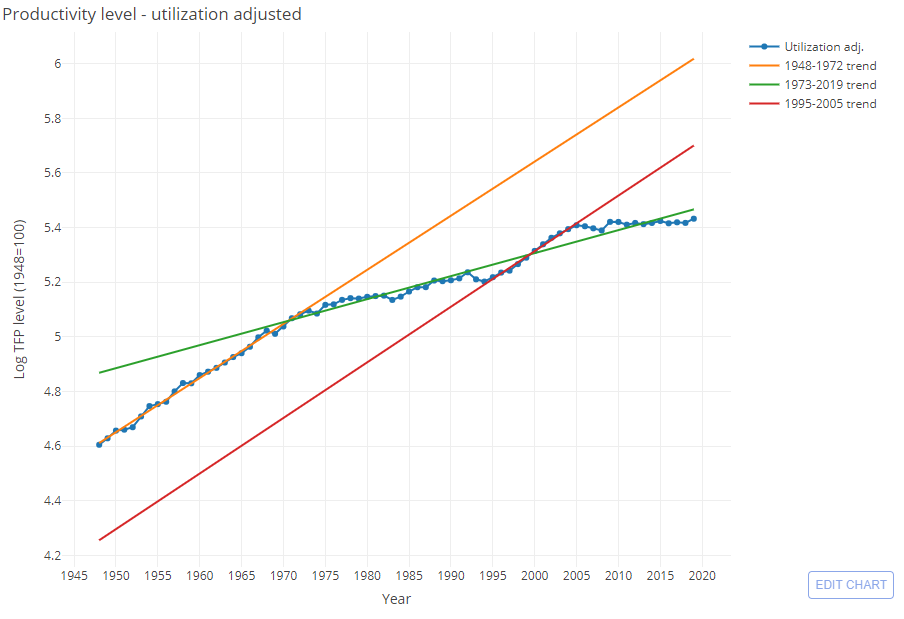

Productivity growth is down, and it’s dragging down economic growth. GDP per capita used to grow 2.25% a year before 1970, but then it grew just 1% per year (on average) afterwards. By some estimations, this is one of the slowest rates of growth ever recorded in American history. About 0.8pp (percentage points) of this come from declining growth in human capital - which makes sense, because the US population can’t go from being 5% college educated (in 1940) to roughly 40% now. The other 0.45pp have to do with productivity. This makes sense, because productivity grew roughly 1.5% a year before the 70s but only 1% afterwards - so the reduction was 33%, not 55%.

Exactly why productivity declined is a gigantic can of worms, where topics like how productivity is measured comes in. Generally, there’s three (or four) big explanations for this observed decline. The first is that actually there isn’t any decline, and we are just shifting productivity from the observable parts to the unobservable ones - say, quality, or non-tradable welfare. Secondly, it could be that something has gone wrong with technology and science, so we’re getting less of a bang for our buck in that arena. Thirdly, there could be a decline in competition in key industries and in the labor market that ia choking out the economy. The slowdown, then, could be good (mostly due to the root causes of each problem) or bad (yet again because of the root causes), regardless of whether declining growth is bad or not.

The other explanation is that a few things have gone wrong, particularly regarding mobility. Basically all of the productivity slowdown comes from declining geographic mobility and declining reallocation of workers and firms. That’s to say, about a third of the productivity slowdown comes from the fact that workers don’t change jobs as much, and about a fifth from people not moving houses as much. Workers not changing jobs has a lot to do with market concentration and with firms getting bigger and older - both of which are linked to aging of the population, plus things like some highly productive companies just hogging whole markets because they were very productive in the past. And geographic mobility is declining because of abyssmal housing policy that’s constraining new homes being built in the most productive cities - but there’s also a trend of people becoming more attached to the places they live in, making mobility decline.

Finally, just under half of the slowdown in productivity (0.2pp) can be attributed to a shift in spending from goods to services. Historically, the goods producing sector has been more productive, and services have just leeched off their productivity growth and gotten more expensive (a phenomenon known as Baumol’s Cost Disease). But because goods producers (agriculture and manufacturing, mainly) have become so productive, they’ve also gotten really cheap, and people aren’t buying more of them. Think of agriculture: basically everyone had to work in a farm in the 1800s. As technology improved, fewer and fewer people had to, and food got cheaper; since people spent less on food (by not buying more of it) the productivity that agriculture contributed to the economy overall got smaller.

Are we measuring correctly?

An explanation for productivity decline can be attributed to mismeasurement. Basically, we’re measuring GDP and productivity wrong, in ways that understate improvements in material quality of life. The richest man on the planet died of a tooth infection in 1836 - how do you add the value of antibiotics to GDP?

Likewise, things like Twitter, Netflix, Wikipedia, or Whatsapp are valuable in similarly hard to quantify ways. The benefits of something like Amazon is hard to tabulate because things like lower waiting times, quality of products, or better book recommendations aren’t easy to take into account. Because these platforms are free, don’t usually have benefits that can be directly quantified like “cheaper prices”, “more sales”, or “more jobs”, and most of their benefits come from network effects, then we’ll never measure productivity growth correctly.

There’s a bunch of problems with this approach. The first is that, even if this was 100% true, it wouldn’t explain the size of the problem. The slowdown is all over the world, and doesn’t bear much relation to how widespread are these new technologies - put another way, places with more Facebook and less VHS should have lower productivity, and this just isn’t true. The same problem appears when trying to control for size of industry or similar characteristics. Secondly, the timing is all wrong - the information revolution of the 90s accelerated productivity first and then declined, in ways that don’t make sense if measurement was the problem. Finally, there’s the simple issue of size - even if all of the above wasn’t an issue, the size of the “new economy” is orders of magnitude too small: the economic losses from declining productivity are 2.7 trillion dollars (roughly 8500 per person in the US) and even the most generous estimates for the consumer surplus created by new tech are one third of this size.

But there’s a much more obvious problem here: why would the measurement gap be a new thing? I don’t think you could argue that all of the gains over the past century of economic progress were measured by GDP, or that a much smaller fraction weren’t, since a lot of new technologies have the same function as the old ones - saving time. Netflix, Spotify, or Wikipedia might be different to, say, the washing machine and the refrigerator, but they had a similar effect: making already existing activities less time consuming and more convenient. To argue that mismeasurement is a new problem you have to find that more of the surplus generated by technology can’t be attributed to economic variables, which I think is pretty bonkers (except, perhaps, for quality increases).

Has science gone bad?

The rate of progress in technology, which is somewhat loosely tied to productivity, has slowed down. The quote above put it best - we seem way off from what we could have accomplished. What happened?

First, some facts. The amount of funding for science, adjusting for inflation, is at an all time high; 90% of all scientists who have ever lived are currently alive and working. Despite this, the total amount of research output we’re getting is the same - meaning each dollar and each brain we’re throwing at scientific issues is less and less fruitful. Nobel Laureates are older and their discoveries happened far longer ago. Inventors are older, less likely to work alone, and less likely to invent something meaningfully different from previous work. This is replicated across fields: mathematics, economics, patents, engineering, agriculture, healthcare, AI, basic sciences, even the humanities. The median company’s R+D money is less productive than it was twenty years ago. This is true for Germany, China, and Japan. Research productivity declined 31-fold since the 1930s, or 5% per year on average.

The big idea here is the burden of knowledge. Einstein once said “As our circle of knowledge expands, so does the circumference of darkness surrounding it”; likewise, each additional speck of light gets less and less effective at actually illuminating anything. The reason brilliant genius polymaths were able to discover everything was that nothing had been discovered. Newton was a physicist, mathematician, chemist, theologian, and even economist; Einstein was mostly just a physicist, and similarly smart modern day geniuses specialize in one precise subfield for decades. Plus, Nobel Laureates being older and their discoveries being from far longer ago might actually mean that more things are being discovered, so we could have a “backlog” of important contributions to get around to awarding.

Because we need to know more and more, the amount of knowledge required to solve a given problem increases very quickly, meaning you need gargantuan teams to actually accomplish anything - and ever since Adam Smith’s pin factory we’ve known that sometimes, too many cooks spoils the broth. There’s also criticism to be made of how academia has a big publication bias that rewards doing very unproductive things, or how universities, government agencies, and the private sector have basically stopped talking to each other with regards to research.

A final explanation is time. Big technologies, like the steam engine, the internet, or electricity take time to spread around. As they spread, extensive investment is needed, and meanwhile inventors and scientists tinker with the technology at the edges. Once this gets big enough, there’s this sort of explosion of productivity, which later peters out once the technology is widespread enough and improvements stop being too big. In the past, we’ve observed similar dynamics: Engels’s Pause, a 50 year stagnation after the original Industrial Revolution; electrification had its big moment in the 1900s, and the internet took 40 years to be even remotely usable. The new technologies that could proper growth to the stratosphere are simply too immature yet - we’re saying that computers will never matter because ENIAC or the Enigma Machine are hard to use.

Clogged up

As I’ve previously talked about, competition across the US economy is down significantly. This has had noticeable effects on innovation, investment, and growth.

The relationship between competition and innovation is a fraught topic in industrial organization, but generally, very competitive industries don’t have enough of it because the margins are too small and the externalities aren’t captured, and extremely uncompetitive industries don’t have innovations because the big firms don’t have any reason to cut costs or improve products. The first case is extremely uncommon, though, so it’s not very empirically applicable.

Besides, there’s fewer and fewer firms going into the US economy, even in sectors where you’d normally expect them to do so - so it’s not an issue of services versus manufacturing again. This ties in with aging, because the future supply of labor is expected to be lower, and results in very few young and growing firms. And this is particularly bad because leading firms invest much less than non-leaders, particularly on R+D.

It’s not just the goods market that’s concentrated. Because of the smaller pool of companies that are hiring, employers have more market power. This results in monopsony, uncompetitive labor markets (because of one big buyer) that, much like a monopoly keeps prices high, a monopsonist keeps wages low. I’ve previously talked about how a tighter labor market (i.e. higher wages, lower unemployment) can lead to more productivity, which might be an explanation for the Industrial Revolution happening in the UK versus the Netherlands or China, but it should be noted this is extremely controversial because of differences in land and labor productivity, for instance, and the whole canning factory of worms that is estimating wages.

Is declining productivity actually bad?

Let’s go back to the breakdown of productivity decline: declining educational attainment, declining mobility, declining turnover, and a big shift from goods to services.

Declining growth in educational attainment could obviously be very good for a simple reason: going from nobody being educated to many people can’t happen that much. Doubling the size of the colleged educated workforce is pretty easy two or three times, but basically impossible after that. Plus, an aging population means that non-educated workers are sticking around longer, and that there’s fewer people to even go to colleges and such in the first place. None of these are bad on their own.

Additionally, if we agree that aging is making the labor market less dynamic, it’s because people are living longer (a good thing, by itself) and that they’re having fewer children. Now, people generally say they want to have more children than they do, and immigration is very good, but this could be just a fact of life, not good or bad. And yeah, bad housing policies cost the economy a bundle (we’ll go back to these things in a bit), but it seems people are also getting more attached to their homes - they were unusually willing to move into and out of certain places (the Southwest, mainly) in the past and then became less willing to, regarldess of cost..

And the shift from manufacturing to services means that we have so many things at such low prices we’re moving on to spending in other people’s time. Exactly what kind of consequences this has is a whole can of worms that gets into topics like inequality and automation, but “people wanting things less and wanting to pay other people for their time more” can in principle be good. People have a basically unlimited demand for things that only other people can provide, so the focus shouldn’t be on bringing the jobs back or whatnot, but rather on making services more productive.

Even the technological slowdown could be a good signal. Robert Gordon argues in his book “The Rise and Fall of American Growth” that economic growth (particularly productivity) declined because the accelerations was a freakish oddity itself - a spurt of new technologies and modes of organization that changed human lives in a single lifespan to a degree that could have only been achieved over multiple centuries in the recent past, and over milennia in times further back. So regardless of the specific items playing a role here, we don’t have anything as big or important as electricity, the Green Revolution, the combustion engine, or antibiotics yet.

Obviously a lack of competition could be bad, but I’ve already talked about how it could be a consequence of things like aging and lower geographical mobility - if those are caused by good things too, then we can’t really do much about them. Plus there’s the issue of “superstar firms”, i.e. companies that got really big by being really productive back in the 90s or whenever and are just coasting now. If technology-induced growth is bound to blow up again soon, the problem would just solve itself, with the lumbering fossils going the way of Kodak and Atari.

Conclusions

So, what can we make of it? Not much. Economic growth, particularly the one driven by productivity, is generally agreed to be good. Having less of it is bad. But maybe we have less of it for good reason - living longer, learning more, cheaper things, knowing too much. Growth being a victim of its own success is clearly not a bad thing, given that it’d point to everything going well, actually.

There are many things we could do to turn this around, though. Competition in many industries is down because of government policies - either too much regulation (say, occupational licensing) or too little. Aging and declining population growth might be solved through immigration. Grants, funding, and incentives could turn science around. And things like protectionist trade policies could discourage manufacturing companies from innovating in the future.

Sources

What is productivity

Shackleton (2013), “Total Factor Productivity Growth in Historical Perspective”

Dietrich Vollrath, “TFP Agnosticism”, 2021

Timothy Lee, “The productivity paradox: why we're getting more innovation but less growth”

Goldin, Koutroumpis, Lafond, & Winkler (2021), “Why is Productivity slowing down?”

The “less is more” hypothesis

Matt Clancy, “Fully Grown: A Review”, 2020

Gordon (2018), “Why Has Economic Growth Slowed When Innovation Appears to be Accelerating?”

Coate & Mangum (2021), “Fast Locations and Slowing Mobility”

Dietrich Vollrath, “Understanding the Cost Disease of Services”, 2017

Are we just measuring it wrong?

Diane Coyle, “Why GDP Statistics Are Failing Us”, US Chamber Foundation, 2015

Syverson (2016), “Challenges to Mismeasurement Explanations for the U.S. Productivity Slowdown”

Scientific slowdown

Patrick Collison & Michael Nielsen, “Science Is Getting Less Bang for Its Buck”, The Atlantic, 2018

Matt Clancy, “Innovation gets (mostly) harder”

Gordon (2000), “Does the "New Economy" Measure up to the Great Inventions of the Past?”

Cowen & Southwood (2019), “Is the Rate of Scientific Progress Slowing Down?”

Bloom, Jones, Van Reenen, & Webb (2020), “Are Ideas Getting Harder to Find?”

Jones (2009), “The Burden of Knowledge and the “Death of the Renaissance Man”: Is Innovation Getting Harder?” - summarized by Matt Clancy here

Jones (2005), “Age and Great Invention”

Matt Clancy, “Are Ideas Getting Harder to Find Because of the Burden of Knowledge?”, 2020

Competition

De Loecker, Eeckhout, & Unger (2020), “The Rise of Market Power and the Macroeconomic Implications”

Gutiérrez & Philippon (2017), “Declining Competition and Investment in the U.S.”

Dietrich Vollrath, “Rising Markups and Falling Productivity”

Brad DeLong, “Robert Allen: The British Industrial Revolution in Global Perspective”, 2012

Pseudoerasmus, “Random thoughts on Allen’s theory of the Industrial Revolution”

Is it bad?

Gordon (2014), “The Demise of U.S. Economic Growth: Restatement, Rebuttal, and Reflections”

Jason Crawford, “The Rise and Fall of American Growth: A summary”, 2020

Great post! I would strongly suggest Carlota Perez as a read on long cycles and how to think about technosocial revolutions and what lessons can be drawn out for our current moment in time. This video seems like a good intro: https://www.youtube.com/watch?v=N0Z8bZSyB-E

As for protectionist policies, do you think there's a brand of temporary protectionism/niche shielding that can be used to encourage innovation? I know you wrote on Twitter on how the East Asian examples aren't really that instructive because the TLDR is "make better firms", but maybe some combination of import substitution with "export discipline" (rewarding companies that export rather than producing for a local market as a way to stimulate competitivity) might be a way forward?