Some thoughts: monetary policy and inequality

Arguing about the Fed increasing or decreasing inequality is beyond the point

There’s been a recent debate on economics-adjacent Twitter about low interest rates and income/wealth inequality. The argument, in broad strokes, is that the Federal Reserve’s loose monetary policy would exacerbate income and wealth inequality by propping up the financial sector and discouraging saving.

The main argument in that sense comes from financial advisor and author Karen Petrou in her New York Times op-ed “Only the Rich Could Love This Economic Recovery”. The argument made is simple: the Fed’s expansionary monetary policies were more effective at boosting the incomes of the rich than of the working class. As a result, inequality increased - because of driving investment to highly speculative assets (like Bitcoin or GameStop stock), propping up the stock market, and increasing the demand for housing. From her article:

Many Americans own stock, but most stocks – 54 percent – are owned by the 1 percent and much of the rest by the next 9 percent.

The same can be said of real estate. Low interest rates set by the Fed spur lending, creating more demand to purchase homes and forcing prices higher. Rising equity is great for existing homeowners, but richer Americans who own property are the ones who benefit most.

What about Americans who are trying to get ahead not through assets, but through saving? Even low-income households are doing their best to save a surprising amount of money. But the Fed’s interest-rate policy robs savers of any interest they might see.

The inequality impact of the invest-you-gain, save-you-lose conundrum is clear.

An similar argument was also made by Lisa Abramowicz on her Bloomberg piece “Fed Decries a Wealth Gap It Helps Perpetuate” on the Fed’s Jackson Hole conference, “Macroeconomic Policy in an Uneven Economy”. The general outlines aren’t particularly different, but Abramowicz also mentions that wealth inequality might also be discouraging investment in productive activities. Larry Summers, a tight monetary policy advocate, also made similar points arguing for the end of QE in a Washington Post op-ed.

I’m not really inclined to go through every claim being made, one by one, and debunking them because this isn’t a Youtube video. Obviously the one big caveat is that housing prices are almost entirely a supply-side problem: if there were more houses being built, housing prices wouldn’t be shooting all over the place.

The first thing to look at is, precisely, why the Fed has such low rates. That’s not a hard question. Modern central banks have generally two “mandates” (i.e. goals): price stability and full employment. In practice, they try to fulfill both by looking at inflation (the first mandate) with unemployment (the second), and the main ways modern banks do this is through their power over interest rates and through quantitative easing, the purchase of bonds and other financial assets from banks and other large investors to provide them with liquidity.

When the economy is weak, and unemployment is high (i.e. now), the Fed responds by having interest rates that are very low so companies can borrow instead of having to tighten their belts, and likewise for individuals. For example, during the Great Depression, the Federal Reserve acted with an excessive level of caution, resulting in a sharp contracion of the money supply that esacerbated existing economic disruptions. From Friedman’s 1968 “The Role of Monetary Policy”:

Finally, monetary policy can contribute to offsetting major disturbances in the economic system arising fromi other sources. If there is an independent secular exhilaration-as the postwar expansion was described by the proponents of secular stagnation-monetary policy can in principle help to hold it in check by a slower rate of monetary growth than would otherwise be desirable.

Friedman is talking about a random event that causes the economy to run “too hot” (i.e., with unemployment that is too low and inflation that is too high) but the opposite isn’t too far off, either. Regardless, the Federal Reserve is a really powerful institution, and thinking that its leadership can’t do anything about a given economic problem isn’t just unambitious - it’s dangerous. From Romer and Romer’s “The Most Dangerous Idea in Federal Reserve History” (2012):

The view that hubris can cause central bankers to do great harm clearly has an important element of truth. A belief that monetary policy can achieve something it cannot—such as stable low inflation together with below-normal unemployment—can lead to the pursuit of reckless policies that do considerable damage.

But the hundred years of Federal Reserve history show that humility can also cause large harms. In the 1930s, excessive pessimism about the power of monetary policy and about its potential costs caused monetary policymakers to do little to combat the Great Depression or promote recovery. In critical periods in the 1970s, undue pessimism about the potential of contractionary monetary policy to reduce inflation led policymakers to do little to rein in the Great Inflation. We have stressed that it is too soon to reach conclusions about recent developments. But, faced with persistent high unemployment and below-target inflation, beliefs that the benefits of expansion are small and the costs potentially large appear to have led monetary policymakers to eschew more aggressive expansionary policy in much of 2010 and 2011. In hindsight, these beliefs may be judged too pessimistic.

Why am I bringing this up? Because, for once, the Fed tackling inequality isn’t something it’s particularly well suited to do. The BIS’s 2021 annual economic report states this very well: inequality has been drive up by a series of changes to the economy (globalization, technology, regulatory and tax code changes, etc) throughout periods of monetary policy that were both too tight and too loose. Monetary policy just isn’t a big part of that story, over time - its main contributions to reducing inequality are controlling inflation (which disproportionately affects lower-income people) and stabilizing the economy during recessions (again, which disproportionately harm lower-income people). From the BIS report:

It would be unrealistic, and indeed counterproductive, to gear monetary policy more squarely towards tackling inequality. Monetary tools, by their very nature, act primarily on cyclical developments. That is why they are well suited to achieving macroeconomic stabilisation objectives. By contrast, a meaningful impact on slow-moving inequality trends would entail sustained application of the tools in particular ways. This would curtail the flexibility of monetary policy to stabilise the economy, potentially undermining the effectiveness of the monetary regime itself. This would be very costly, not least because the macroeconomic stability that those regimes can deliver is precisely what is most conducive to equitable income and wealth distributions.

But there is also another problem: monetary policy was, and has been, too tight, not too loose after the Great Recession. The Fed decided to raise interest rates too early, when unemployment was still high and inflation was below target, due to fears of higher inflation. Not paying enough attention to the Fed was described as Obama’s biggest mistake, and people like Greg Mankiw and Scott Sumner (a republican, at that time, and a libertarian respectively) argued against the move.

In fact, US GDP actually fully recovered from the Great Recession in 2018, in terms of getting GDP at its full potential level (see graph above). This means that, for 12 years after the Recession, the US wasn’t producing as much as experts thought it could. And if you look at the trends from before the Recession, the picture is even starker - the US economy was 20% below its pre-2007 trend in 2020 and the gap is only going to get wider. In 2007, the Congressional Budget Office estimated that the US economy would grow by a about a third in the following ten years; instead, it grew just 18.5%.

This slow recovery also affected the labor market, where the Federal Reserve raised rates even when unemployment was above 6% and many other key indicators, such as employment-to-population and labor force participation, took until the Trump era to recover as well. For example, the US would have about ten million jobs more than it would given current predictions just by getting each age group’s employment levels to the levels they were in the early 2000s. This sluggish recovery of the labor market happened for a variety of reasons, but “insufficiently tight monetary policy” was not one of them.

And my friend Joseph Politano has written about this as well, pointing towards the sluggish recovery in the labor market working against inequality reductions, not in favor of them. And during the loose monetary policy, tight labor market Trump Era, wages increased more for low wage workers than they had since the Great Recession. Plus, left leaning economist Michael Kalecki wrote that full employment and a tighter labor market would lead to higher profits for business owners and to more political power for workers (as well as income gains), neither of which seems bad.

Also, according to a Brookings report, after the Recession, the Fed’s policies that propped up housing prices benefitted the middle class far more than the rich, since housing is a far bigger share of their assets. And additionally, even if the Fed might have increased inequality by doing monetary stimulus, the resulting stagnation from not doing any stimulus would have been far worse - since an inequality-reducing fiscal stimulus would be beyond the Fed’s purview.

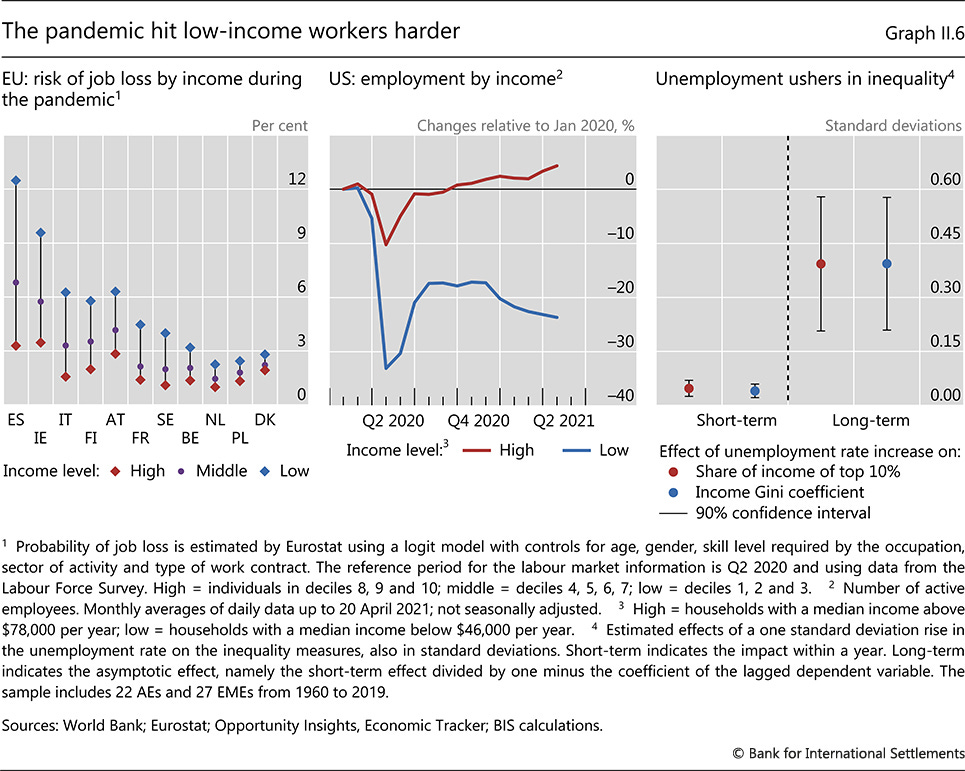

Going back to the BIS report, much is said about the effects of monetary policy on inequality. Inflation increases inequality, because the rich have plenty of options to protect their income against it while the poor, whose wages rise far more slowly, do not. But employment is where the bulk of the effect comes into play: recessions hurt the working class far more than other groups. And additionally, since the rich save more money and have been hurt far less by recessions, they have experienced a “savings glut” that brought interest rates down - meaning that people might be getting the correlation precisely backwards.

In conclusion, monetary policy isn’t a good tool for reducing inequality, isn’t the reason inequality is going up, and the drawbacks of tighter monetary policy would by far exceed their benefits. To go back to the quote from Romer and Romer, it is both dangerous that Central Banks try to do things they can’t do, as it is dangerous that they don’t do things they can. The Fed can reduce inequality by keeping inflation in check and by strengthening the labor market - not by tightening monetary policy for no apparent reason other than to “own” the rich.