Inflation alert!

In this special edition, we tackle one question: why was the March inflation rate 5%?

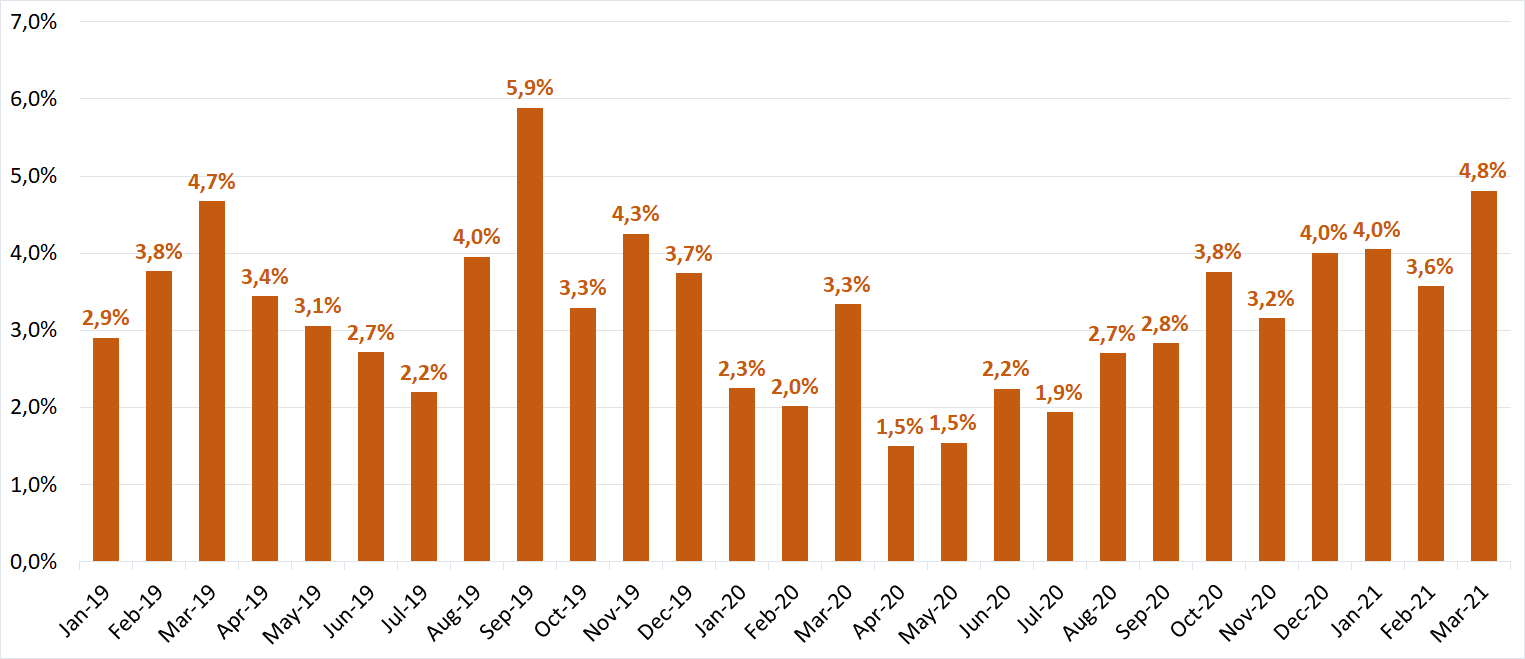

The March CPI figures came out yesterday, and they’re not pretty. National inflation was 4.8%, the highest value since September and the third highest in three years. Annually, it was 42.6%. Annualized (i.e. if this pattern was repeated every month) it would be slightly below 75% this year. Why did this happen? And why is it so unusual?

Breaking it down

How did we get to nearly 5%? Looking at spending items, we get our first clue. Not every item increased at the same rate, and not all of them matter the same. For example, a 3% increase in food and beverages is much more important than a 3% increase in communications. Inflation measurements adjust for this by weighing each category by its share of the consumption of an average family, so items that aren’t as important don’t receive as much weight as the core of each household’s monthly purchases.

Of the monthly figure, the biggest increase was in edducation, increasing 28.5% last month (that’s just in May). However, since spending on education is just 2.3% of the total education basket, it only added a whopping… 0.7% to monthly inflation. A big figure, but think of it this way: if food and beverages increased that much, they would add ten times that amount to the monthly rate (7.7%) and monthly inflation would be 11.5%. Almost half the monthly rate was just a 4.6% increase in food and beverages (one sixth of the monthly rate) and an eye-popping 10.8% hike in clothing prices (an almost equal figure to food and beverages).

Regionally, it was similar across the country, with the poorer Northwest and Northeast having 3.3% and 4.2% increases respectively, the center Pampas and Cuyo region having price increases of 4.8% and 4.3%, and the southern Patagonia having a mild 4.1% hike - differences between the regions are mostly due to different weight of the various categories in them, and different management of public utilities. The hardest hit region was the Buenos Aires Metro Area, home to a third of the country, which had price hikes of 5.2% in March.

On a bigger scale, you can break the CPI into three categories: core inflation, seasonal inflation, and regulated price inflation. Let’s start by the end: the Argentinian government has a lot of power over certain prices, most importantly utility bills, but also telecommunications bills and health insurance premiums. Regulated prices increased 4.5% in March, mostly due to big hikes in fuel and health insurance - and they haven’t increased much since last year (15% in 2020, vs 37% for the general level). Seasonal prices correspond to products that increase or decrease based on the time of the year, such as fruits and vegetables. They have seen the fastest growth of all, growing 7% last month and 64% in 2020. The core inflation rate is the most important of them all, and it basically encompasses all the other products - it’s very frequent for policymakers to focus on core inflation, because it tends to be the one that reflects the “real trends” of the economy.

Why did this happen?

One item that is not in the exchange rate but does feature heavily in inflation discussions is the exchange rate between the US dollar and the peso. In general, when the exchange rate goes up, so does inflation. Conceptually, we can think of it in two (very simple) ways. Number one, big hikes to the US dollar increase costs for businesses that require imports or that export part of their production. Number two: abrupt increases in the dollar point to something going “badly” in the economy, and thus inflation expectations go higher - meaning people start acting like inflation will get higher, which often means doing things that actually increase inflation.

That, combined with regulated prices, more or less explain the dynamic until… just now. Except for the last month, the US dollar has behaved more or less peacefully, with highly managed devaluations. You can very clearly see the breakdown of that relation in the graphs above, plus the monthly rates above 3% started before any big regulated hikes. So… what gives?

The first part is that the official exchange rate is under control, while the parallel rates are not. While the government charges $97 for a US dollar, the black market will ask for $140-150, meaning that both of these figures weigh on inflation expectations. For example, in late September all the relevant rates shot up, reaching highs of $195 by mid October… and the inflation rate grew 1 full percentage point, from 2.8% to 3.8%.

The second part is that the government has massively expanded the monetary base in the past 12 months, by 1.2 trillion (or about 55%). You don’t have to be a monetarist hardliner to think that, once COVID restictions were lifted, that would have an impact on the price level. Once you consider that effects appear over time, it starts clicking. Additionally, the government’s inflation plan has mostly consisted of ordering companies to lower prices, ordering companies to produce more, and fining companies for increasing their prices, plus sending out inspectors to verify adherence to price control agreements. This is… not effective (obviously).

So, as a summary, you have a terrible monetary policy that is pushing inflation upwards, and national authorities that simply refuse to acknowledge they could be a cause of the problem and instead blame evil corporate greed on a purely fact-free basis. Either the government comes to its senses and starts rebuilding a monetary programme that isn’t based on paranoid conspiracy theories and “heterodox” nonsense, or things get really bad fast.