Convergence, big time

Rich and poor countries have gotten richer. But have their incomes gotten closer?

Mr Solow and the neoclassics

The most common textbook model used to explain per capita economic growth is the Solow Growth Model, named after its creator, Robert Solow. Without going into too much detail, the model is centered around population growth, technology, and savings being constant across time and around production depending only on labor and capital (workers and machines, so to speak).

What’s important is that the state of the economy doesn’t depend on any “contextual” variables, but rather on a handful of structural parameters - that is to say, on things like the percentage of income that is saved, how quickly capital needs to be replaced (depreciation), and the rate at which technology grows. These factors are obviously not exclusively economic, but depend on a variety of factors: institutions, government policies, etc.

Convergence 101

The model has a very interesting implication. If you look at countries with similar variables, then the ones who start further away from the steady state (we’re assuming they start poorer and not richer) should grow faster than those who start very closely. This happens for a very simple reason: since factors of production have decreasing returns (they get less effective the more of them there are), so the more capital per worker you have, the less growth each additional unit “makes”. This “catch-up” is known as convergence.

There’s two basic kinds. Imagine a bunch of countries that are very similar to each other in culture, government, resources, etc. It would be reasonable to assume they have similar savings rates, depreciation, and technological advancement - so their steady states are probably very similar. As a result, they will experience absolute convergence, which means they will reach (roughly) the same steady state - a very strict definition. On the contrary, if there is no specific reason for them to have the same “ceiling”, then they might still show convergence - conditional convergence, which just requires countries to start slowing down as they get richer.

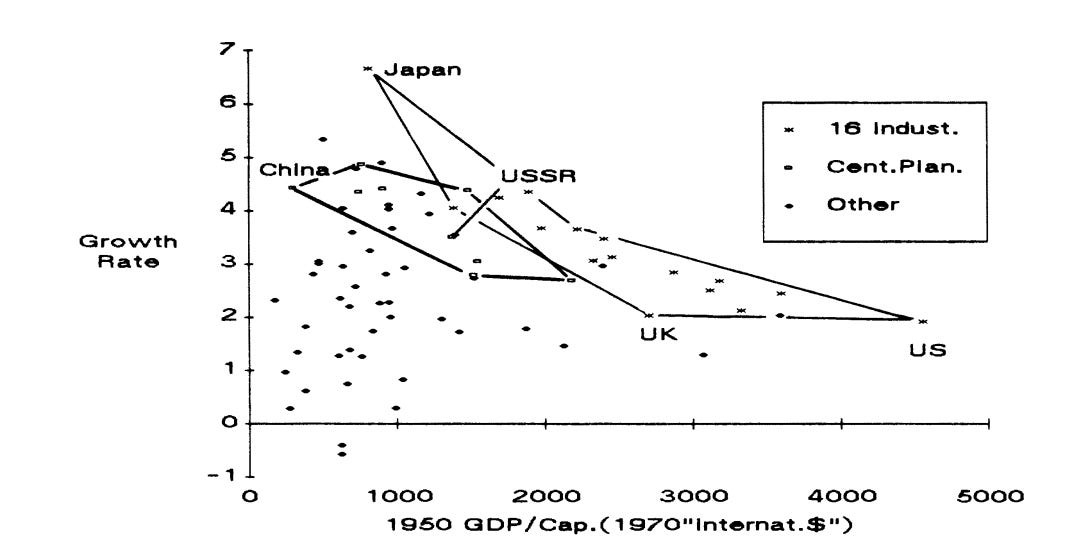

Absolute convergence is pretty rare - countries just aren’t similar enough (more on this later, though). Conditional convergence seems at least possible, however - rich countries might eventually “exhaust” themselves, while poor countries don’t. Does it actually happen? Kind of. In the graph above, you can see basically three “clusters” of countries. The first is a group that has clearly shown convergence - rich countries like Japan, the US, etc. The second group, formed by centrally planned economies, has shown some convergence of its own. The third group (everyone else) is a huge mess.

Countries, when they converge, tend to form convergence clubs, that is, they tend to form groups of countries to converge between each other. This happens for a variety of reasons: they are more similar in “culture”, they adopted similar policies, etc. Rich countries are very obviously a convergence club, and so were centrally planned economies. Another fun example comes from the United States themselves: non-Southern states show one trend, Southern states show another one.

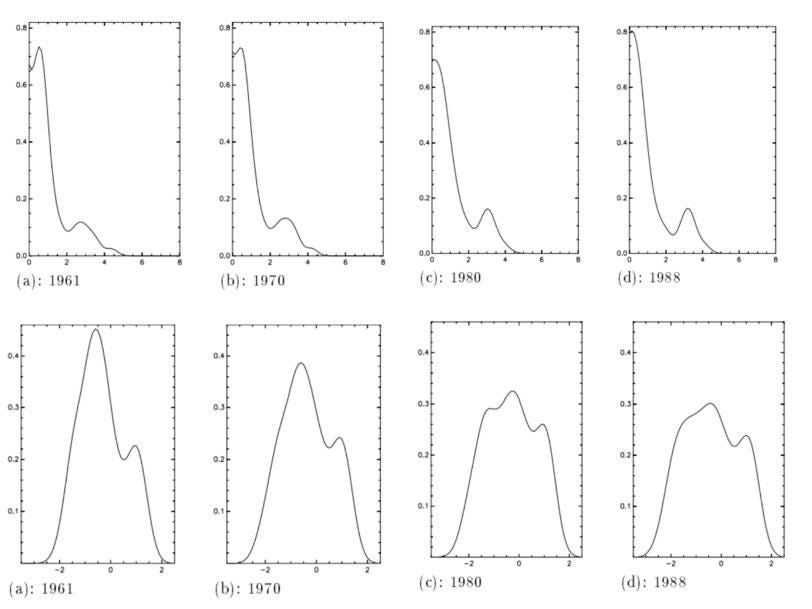

Something that is quite interesting is that, by the 1990s, two “big” clubs were formed: rich and poor countries. Rich countries had converged, and it actually seemed the poorest countries on Earth were converging - to a “bad” state, where they remained stuck. Eventually, if that trend held, it would mean that all countries would either join the poor, no growth group, or the rich, no growth club - the “twin peaks” distribution.

The 90s Convergence Wars

Convergence was a very hot topic in the 1990s, with two central questions: was it happening? And why?. We have outlined the major facts by then: convergence between rich countries but not with poor ones. Let’s look at the logic.

Let’s start with rich countries, long long ago. Some of them, like European nations, have been very rich for a long time, but others, like Japan, Chile, or Israel (not to mention other parts of Europe) were various degrees of poor before becoming rich. But this is clearly tautological, because there are only three possibilities. If you take countries that are rich now vs where they were in 1870, then they started out rich and grew just enough to remain rich while other countries caught up, or were poor and grew very quickly until they were rich as well. The third alternative, which is vanishingly rare, are rich countries that ran themselves into the ground and stopped being rich at some point in the last 150 years (one of the only such examples is, somewhat hilariously, Argentina).

To take a look at poor countries, which have much lower quality data, we should define a lowest possible bound for what their GDP per capita is. Many of these were, in the 1870s, colonies of the rich European countries, where most people were either slaves or subsistence farmers. Many of them remained incredibly poor ever since, in fact. The lowest reasonable income that a person can have and still not be severely malnourished is about 250 dollars per capita. Without getting too much into methodological differences, we can see that almost all countries should have started there, because cavemen didn’t have access to machines or trade. At some point, some countries needed to have taken off, while others didn’t.

Between 1870 and 1985, the income of the richest countries roughly quadrupled, so to stay even all countries should have had a GDP per capita of about 1,000 dollars - and plenty didn’t. A country starting at the lowest bound could have reached the US by growing about 4.2% per year, on average - high, but not impossible, since plenty of economies (11, mostly East Asian) accomplished it during the 1960s. But this is not representative of most developing countries, since roughly the same number had negative economic growth in that 30 year period, about three times that number grew less than 0.5% a year, and 40 developing countries grew less than 1% - so out of 108 developing countries, 84 grew less than a quarter of the amount they should have to converge.

But there is something else we need to consider: human capital. Workers that are better trained, more educated, and healthier will punch above their weight in terms of “effectiveness” - in a way that is very hard to measure directly. If you split capital into physical capital and human capital, then the Solow model does actually result in conditional convergence - once countries invest a bare minimum in their workforce, the results are much better. Thus, after accounting for different policies in healthcare, education, etc, then countries with a minimum level of schooling should start getting traction.

Then there’s the question of policies. Growth rates are simply too unstable to be predicted by such long term characteristics - a lot of developing countries suffered slowdowns in growth without experiencing substantial changes. We have already pointed to education as one potential culprit, but even then it doesn’t tell the full story. But what about government policy, conspicuously absent from this debate? A lot of poor countries have (had) very bad policies: high tariffs, export controls, centrally planned economies, weird foreign currency manipulation. In countries that didn’t adopt such policies, growth has been much higher, and convergence (somewhat) possible - openness had a premium of a staggering 2.5% a year, and 3.4% a year for poor countries. Besides from the fact that policies aren’t exogenous (so countries that don’t adopt them might be failing elsewhere too), convergence still didn’t happen after “opening up” their economies - and in many cases, reforms simply failed due to bad luck.

So the big convergence fight of the 1990s was sort of a dud: no consensus was reached, and no conditions to achieve it were discovered. As a TL; DR of the findings of the era, we see that:

rich countries converged with each other in absolute terms

the poorest countries converged with each other as well

there wasn’t much convergence between rich and poor countries

human capital is important, and so are good policies, but they don’t tell the full story

Convergence after the 1990s

What happened after the groundbreaking research of the 1990s? A lot, it turns out. For starters, incredibly entertainingly, US states stopped converging between each other (probably due to bad housing policies).

During the late 1980s and 1990s, in fact, plenty of developing countries did adopt the reforms advocated - to various degrees of success. There were some big hits (China, India, Chile) and some big busts (Russia and, again, Argentina). It is very hard to see the impact of any specific policies on growth - for good reason: most countries opened up after the 80s, when the benefits of doing so got much, much smaller.

A 2020 paper by Johnson and Papageorgiou states:

Our reading of the evidence, then, is that recent optimism in favor of rapid and sustainable convergence is unfounded. The last two decades of an unprecedented wave of growth in many LICs and emerging markets led to many analysts claiming prematurely, in our view, success (…) Many observers are led to believe that “this time is different.” We have come to the conclusion that with the exception of a few countries in Asia that exhibited transformational growth, most of the economic achievements in developing economies have been the result of removing inefficiencies, especially in governance and in political institutions. But as is now well known, these are merely one-off level effects that, while not unimportant, and in fact necessary in the process of development, nonetheless do not stimulate ongoing economic growth.

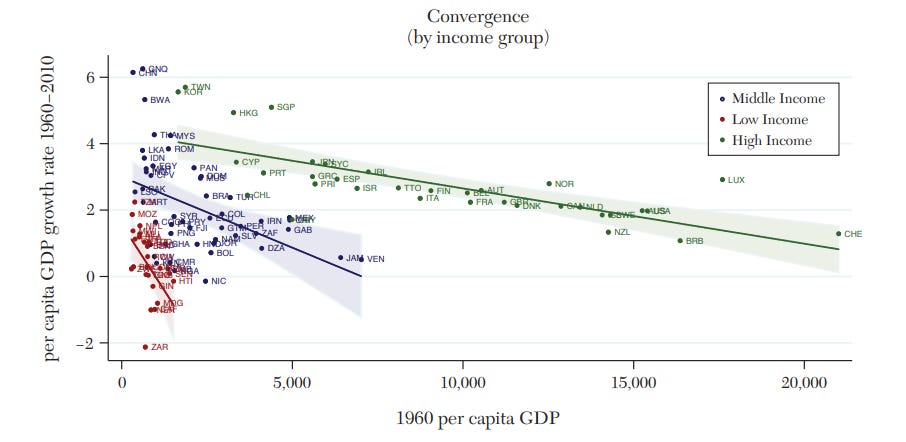

So not very encouraging… except… “an unprecedented wave of growth in low income countries”? That doesn’t sound like nothing. Starting in 1995, there was a big change: countries started converging, and not only in conditional terms - there was absolute convergence. This happened for two very broad reasons: rich countries slowed down, and poor countries sped up. Whether you measure between countries or within them, weighing people, and including or excluding India and China, the results are clear: at some point between the late 80s and mid 90s, convergence came “back” with a vengeance.

At the lowest end, of the countries the World Bank considered “low income” in 1990, two thirds have grown faster than the average. And this is not “just” India and China either - this has been a pattern across developing economies. For middle income countries, the prospects are even higher - over 80% have done so. In fact, “the middle income trap” that defines the issues for developing countries might not even be real at all, since it either implies no convergence of any kind, or it implies that middle income countries can’t “graduate” to be rich (mostly caused by bad definitions of middle and high income in the first place). There seems to be, in this day and age, no penalty in growth for being middle income at all.

The future of convergence

From 1990 to 2007, developing economies grew 2.5% faster per year than rich ones - and starting in 2000, the gap actually widened, to 3.5%. But since the late 2010s, many developing economies (especially in Latin America) slowed down. It seems that, in many places, the original “wave” of convergence might be running out. Part of this is simple: poor, badly organized, inefficient economies can squeeze a lot of growth from just getting everything in order. But once the problem of allocations is (somewhat) fixed, it is possible for growth to decelerate.

Additionally, there is also a worrying trend in developing economies to backslide into authoritarianism. As I pointed out last week, non-democratic regimes simply do not have the incentives to invest in the kind of things that make growth actually possible (education, healthcare, etc). Furthermore, the authoritarian isolationists of the first world pose a threat to third world economies too: trade and immigration have benefitted, not harmed, developing nations.

An additional risk to consider is climate change, which will affect developing countries in tropical areas, with less available natural resources and worse infrastructure, much more than rich ones. This doesn’t mean developing countries face a tradeoff between growth and sustainability, because developed countries don’t either: the technologies to grow sustainably already exist.

Lastly, and going back to the “twin peaks” prediction: it has mostly died out. The presence of convergence between rich and poor countries (measured by countries and people, and within countries too) seems to signal that the future of the global income distribution will not be two diverging peaks, but rather a right-shifted bell curve.

Sources

Special thanks to Noah Smith for pointing me towards some of these sources on Twitter.

Baumol (1986), “Productivity Growth, Convergence, and Welfare”

Barro (1991), “Economic Growth In A Cross Section of Countries”

Ben-David (1997), “Convergence Clubs and Diverging Economies”

Mankiw, Romer, & Weil (1992), “A Contribution To The Empirics Of Economic Growth”

Baker, Rosnik, & Weisbrot (2006) The Scorecard on Development: 25 Years of Diminished Progress

Johnson & Papageorgiou (2020) “What Remains of Cross-Country Convergence?”

Patel, Sandefur, & Subramanian (2021) The New Era of Unconditional Convergence

Dear Maia,

Thank you for this excellent blog, and growth on graph 8 is misspelled

Awesome work, loving this newsletter...