Burning money on burning gas

What should Argentina do about its utility bills?

One of the most politically contentious topics in Argentina is the subject of utility bills, both between the two main parties and within the current government. The scale of conflict inside the administration was such that, when the Economy Minister wanted to fire the Undersecretary for Electricity (basically for what amounted to “incompetence”), this set off a one week political crisis that almost ended with the Minister being ousted instead. Plus, during a record heat wave in Buenos Aires in mid-January (of 2022), large chunks of the city were left without power for hours at the same time as temperatures reached 100 (or 50, if your country is normal) degrees.

What even is the problem?

The situation is particularly serious because of the scale of the problem. Between 2003 (or so) and 2015, inflation surpassed by far the modest or non-existent adjustments on utility prices, resulting in the level of spending on such items ballooning to between 2% and 3% points of GDP - and explaining 74% of the fiscal deficit by 2015. This tenfold difference was reduced between 2016 and 2019, although at a great political cost. But by 2020, with the Peronists back in power and the pandemic raging on, utilities didn’t increase in the first year of the pandemic (versus 36.6% inflation) and only grew 9% at most in 2021 (versus 50.9% inflation). Not great!

Microeconomically, this isn’t really a hard story. Government imposes price control on thing with no possible substitutes. Thing becomes unprofitable to make. Costs rise, because of inflation. Companies that make thing adjust by slashing all their expenses within inches of their life. Quality gets worse. Not a particularly new tale - if you have a service where pretty much the only thing to slash is investment, investment will get axed, reducing (future) supply at the same time as increasingly lower relative prices incentivize excessive demand. Not a recipe for stability.

You can also find lots of other faults and flaws with controls on utility bills. Incentivizing excessive demand of energy, which is primarily produced through fossil fuels, is not an environmentally sound strategy. If you spend more than a milisecond thinking about who has and who hasn’t electricity, water, and particularly cooking and heating gas in their houses, you find that subsidies are pro-rich to the point that they verge on being regressive. Even if they weren’t, it’s not particularly clear why the path forward for redistirbution should be mucking around with relative prices and not just giving poor people money to make up the difference.

Printing money to burn gas

But the key problem here is macroeconomic: imagine there is no microeconomic distortions, or externalities, or bad targeting of indefensible “welfare”. Then what would be all the fuzz about? Well, that the government spends a lot of money on something implies it has to pay a lot of money for that something too. And in Argentina, “how do you pay for it” is the key question for macroeconomic stability.

I quote this piece (related item by me in Spanish) every week by now but still - let’s look back over at inflation. The traditional story (i.e. Friedman’s “always and everywhere”) is too much money chasing too few goods. Too much spending (“aggregate demand”) and too little production (“aggregate supply”). Not many actors in the economy have the kind of firepower to keep demand constantly above supply, so it’s basically almost exclusively the government’s responsibility.

High inflation is a horse of a different color, though. There’s not really a threshold on what constitutes as “high”, but let’s say double digits for many years. Normally, the government can pay for spending by raising taxes, cutting other parts of the budget, or borrowing money. Basically everywhere, the government borrows money from the private sector, but a handful of times the Treasury decided to borrow from the Central Bank directly instead - aka “printing money” to pay for things. To the contrary of what innumerable TikToks will tell you, you can’t just do that - you’re just adding money to the pile of money chasing things.

The situation where the Treasury can boss the Central Bank around is called fiscal dominance, and while it doesn’t necessarily involve funding the deficit, it’s generally (and correctly) considered bad. This is due to the fact that the Central Bank cannot actually control inflation, its main job, since it has to keep in mind what the government needs. If the Central Bank wants to print less money, but nobody wants government debt to pay for the deficit, then it has to step in - so inflation goes up. This plays out in some very intereresting ways, but that’s neither here nor there.

Because utilities are directly incorporated into the consumer price index, and because they factor into the costs firms face, then whether or not increasing utilities is actually inflationary or disinflationary depends on which effect is bigger - the effect of utilities on prices directly, or the effects of fiscal and monetary policy?.

The answer depends on the size of the spending on utilities, the weight on the price level, and the degree to which the deficit is monetized. It is inevitable that the adjustment of relative prices increases inflation in the short run (after all, a price goes up) but if the degree to which subsidizing utilities explains the deficit and if the deficit is heavily monetized, then inflation first goes up and then is reduced permanently, absent any other changes. Otherwise, inflation just returns to its previous level once all prices have adjusted.

Inside and out

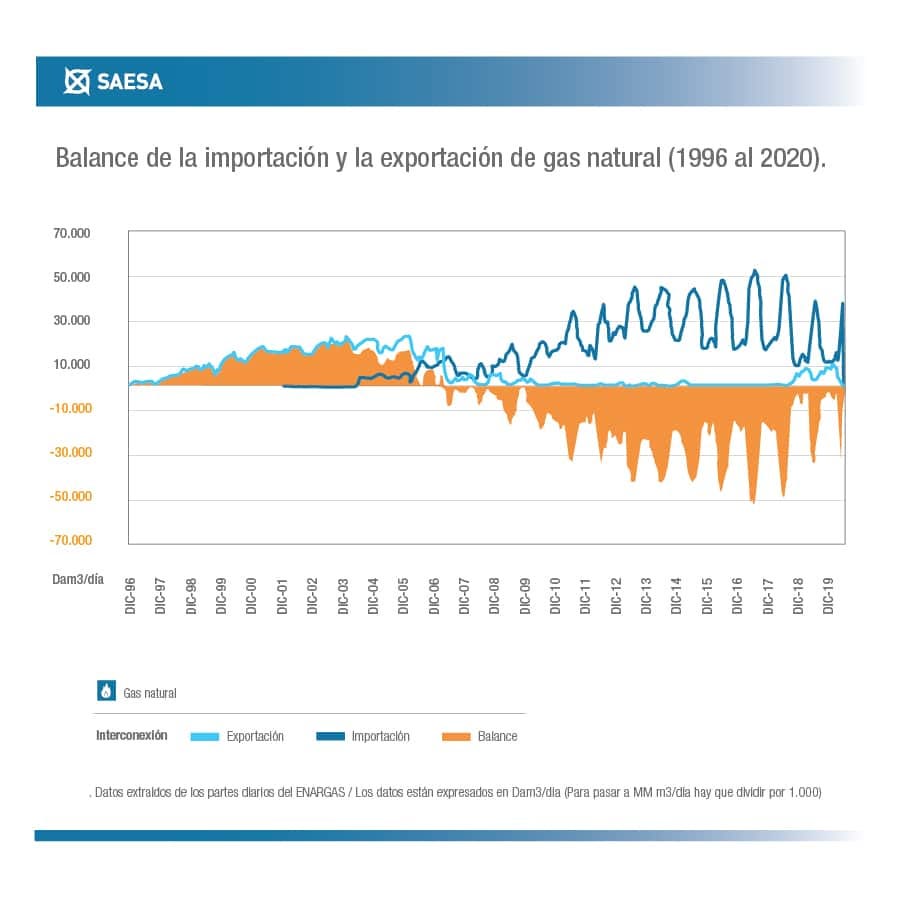

But there’s another really interesting macroeconomic issue that plays out here: the trade balance. Argentina’s power grid is primarily powered by natural gas, a large chunk of which is imported. Under strict price controls, production is disincentivized and consumption is incentivized, meaning that imports must grow. Does this have a bearing on macroeconomic stability?

Yes, actually. Argentina is a profoundly dollarized economy - meaning that whatever happens in the currency market has significant effects elsewhere. Firstly, people demand US dollars to save and invest, because the dollar generally tends to hold its value across time. In addition, the dollar acts as a nominal anchor for the economy, meaning that it acts as a reference point for expectations of future inflation. Thirdly, the cost of imported items is directly linked to the US dollar, meaning that a devaluation impacts costs and therefore can raise prices. All this, in turn, means that sudden movements in the exchange rate imply sudden movements in inflation as well.

So far, the government undertakes policies that increase imports a lot. Holding exports constant (they actually decrease, because of the drop in natural gas production), this results in a larger trade deficit. If the only part of the balance of payments is the trade balance, then the result is reflected one-to-one in an equal drop in Central Bank reserves. Under a floating exchange rate, this results in a devaluation. But what if you peg the exchange rate?

A pegged exchange rate is an interesting creature, since its main goal is to actually anchor inflation expectations at any given level. But if it could do it flawlessly, no countries would have inflation - so what goes wrong? Basically, to defend a currency peg, the Central Banks needs to be willing to buy or sell reserves to clear the market. But since reserves are not unlimited, and Central Banks generally publish data that lets you estimate them, then traders and savers alike can have a general idea of when the Central Bank “runs out” and has to devalue the currency because it can no longer clear the market at the agreed upon peg. This is known as a balance of payments crisis, and they are generally bad. In a perfect, frictionless, no-uncertianty world, it causes a one-time increase in the price level (i.e. “transitory” inflation) and nothing else. But if inflation expectations get thrown off track by the devaluation, then inflation increases permanently.

Conclusion

Microeconomically, the case for aggressive checks on utility prices is paper-thin. At a macro level, with some caveats, it is even weaker. The government printing money to pay for things is generally understood to be a big cause of inflation. So printing more money to pay for an increasingly larger share of a given product results in a permanently higher rate of inflation. Additionally, policies that purposefully worsen the balance of payments at the same time the currency is pegged eventually result in at least a temporary burst of inflation, and perhaps even a permanently higher rate depending on what occurs.

The macroeconomic situation is, was, and for the foreseeable future will be complex. But pursuing policies with basically no benefits and which pose massive risks to worsen the country’s key problem is not a smart path to follow.

Sources

Sebastián Galiani, “Impacto de las tarifas energéticas sobre el bienestar de los hogares”, Foco Económico, 2018 (in Spanish)

The fiscal side

Sargent & Wallace (1981), “Some Unpleasant Monetarist Arithmetic”

Canavase & Heymann (1989), “Indexación, rezagos fiscales, e inflación” (in Spanish)

Navajas (2015), “Subsidios a la energía, devaluación y precios” (in Spanish)

The balance of payments

SAESA, “Importador y exportador: la relación de Argentina con el gas natural”, 2020 (in Spanish)

Fernando Navajas, “Los déficits gemelos en energía”, Foco Económico, 2012 (in Spanish)